New businesses spring up all the time in the U.S. But which ones have the greatest ability to become big? A method developed by MIT researchers, based on an empirical study, projects the growth potential of high-tech firms with new precision — and could help local or regional policymakers assess their growth prospects.

“A central question in evaluating the impact of policies toward business creation, startups, and innovation, is simply how to measure the kinds of entrepreneurs who are likely to build growth businesses,” says Scott Stern, the David Sarnoff Professor of Management at the MIT Sloan School of Management, who led the study. For all the theorizing about the subject, he adds, “There has historically been a big gap, in terms of how to measure and do analytics in a systematic way.”

But now, based on a uniquely comprehensive analysis of businesses in California, Stern and his colleague Jorge Guzman, a doctoral candidate at MIT Sloan, have created a richly detailed picture of what characteristics high-growth tech firms have, and where they exist. The study is summarized in a new paper — titled “Where is Silicon Valley?” — being published today in Science.

Among other factors, firms that formally register, seek capital investment, and make news early in their lives have higher growth potential. That much might seem intuitive — but even a firm’s name, Stern and Guzman found, offers a solid hint of its growth potential. For instance, a business whose name includes the name of a founder does not generally expand as much as other types of firms.

“That combination [of factors] turns out to be a very useful diagnostic for separating out the types of businesses that have a reasonable chance of growing, versus those that are much less likely to grow,” Stern says.

By assessing what it calls the “quality” of startups, and not just their quantity, the study also highlights which towns are home to startups with higher growth potential. In California, the municipalities of Menlo Park, Mountain View, Palo Alto, and Sunnyvale top this list, in that order, with startups having characteristics that are associated with offering an IPO or being subject of a large acquisition, at about 10 times the state average.

From Silicon Valley to Massachusetts

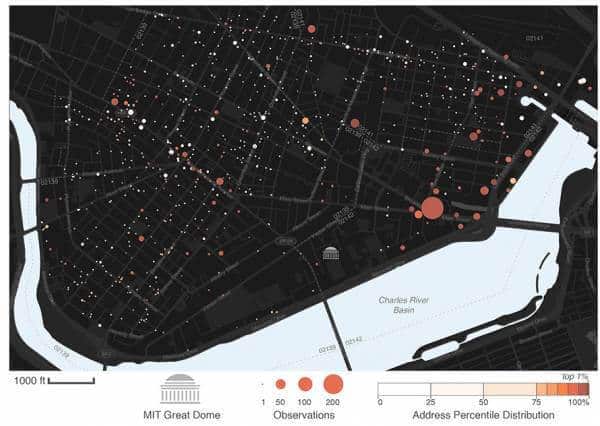

Stern and Guzman are in the process of studying Massachusetts in similarly granular fashion; they are releasing a working paper, as well as initial data visualizations of Massachusetts, to complement the work on California.

To conduct the study, Stern and Guzman used a comprehensive list of new firms from California’s official business registry over the years 2001 to 2011. For 70 percent of the firms, they were able to correlate a series of features that characterized high-growth firms over the period from 2001 to 2006; they then used those findings to test their results against the outcomes of the other 30 percent of new firms in the same period. They also tested their model against new firms registered in the years 2007 to 2011.

One thing Stern and Guzman observed is that even in tech epicenters, the majority of newly-registered businesses do not revolve around technology.

“Even in a place like Palo Alto, or Cambridge, Massachusetts, most of the new businesses are retail-oriented small businesses that are not very likely to grow,” Stern says.

Stern emphasizes that the study is not meant to minimize the value of these smaller businesses, which are integral pieces of local economies — pizzerias, dry cleaners, and many other types of firms. But in filling local niches, such businesses have an inherent ceiling on their growth.

“All of those are very legitimate businesses and important for the local economy,” Stern says. However, he adds, “The intention and potential of those businesses is different, and we can use analytics to evaluate that in roughly real time.”

Those local businesses, incidentally, are the ones most likely to bear the name of a founder, especially in areas like food and various services industries; the name implies a personal touch for regular customers. “That’s almost declaring the intention of the founder,” Stern says.

By contrast, the study includes a list of hundreds of words commonly found in the names of high-growth, high-tech firms.

Shaping policy

While it might seem clear that a pizzeria will rarely grow the way an ambitious tech firm might, it is much harder to make aggregate assessments of the growth potential of a whole set of firms in a given place.

But by using the methods Stern and Guzman have developed, local, state, and regional planners can make progress on that front, and evaluate whether they have a mix of business activity that offers tech-based growth potential. As such, other scholars say, the study can help inform economic policy design.

Aaron Chatterji, a professor at Duke University who was not involved in the research, notes, “A lot of times in policymaking, we know how to count things. … It’s much, much harder to delineate [in terms of] quality.” Stern and Guzman, he adds, have “really tackled a question people care about. … I think it’s going to go over well with the policy community.”

To be sure, many industries, not just technology firms, have growth potential. In another research paper Stern co-authored that was just published, he lays out findings that many cities and regions can achieve growth by establishing clusters of firms in a variety of industries. In both papers, Stern says, an important motivation is to provide policymakers with data tools to better craft new measures.

“It is very difficult to manage the entrepreneurial ecosystem if we cannot measure the entrepreneurial ecosystem,” Stern says. “While our work is a first step, we believe that policymakers and practitioners and researchers would benefit from being able to assess … the combined entrepreneurial quantity and quality in a given region. What we want is to really create new real-time economic statistics.”